Market Recap

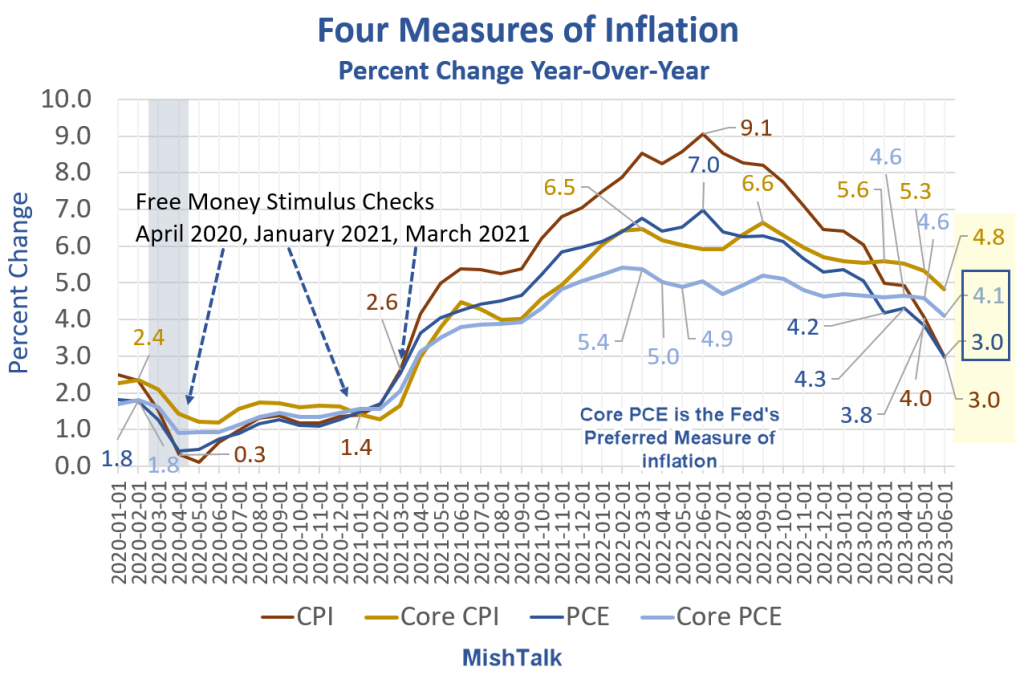

Another downside surprise in US core Personal Consumption Expenditures (PCE) price index paves the way for Wall Street to resume its rally last Friday (DJIA +0.50%; S&P 500 +0.99%; Nasdaq +1.90%) as promising inflation progress reaffirmed market expectations for a Fed rate pause.

The core PCE index for June registered a 4.1% year-on-year increase (versus 4.2% expected), which is its second consecutive month of below-consensus read. Another closely-watched Fed’s inflation indicator, the 2Q employment cost index, also showed progress with a 1% read versus the 1.1% consensus. Overall, the confluence of moderating inflation and resilient US economic conditions continues to be supportive of soft-landing hopes.

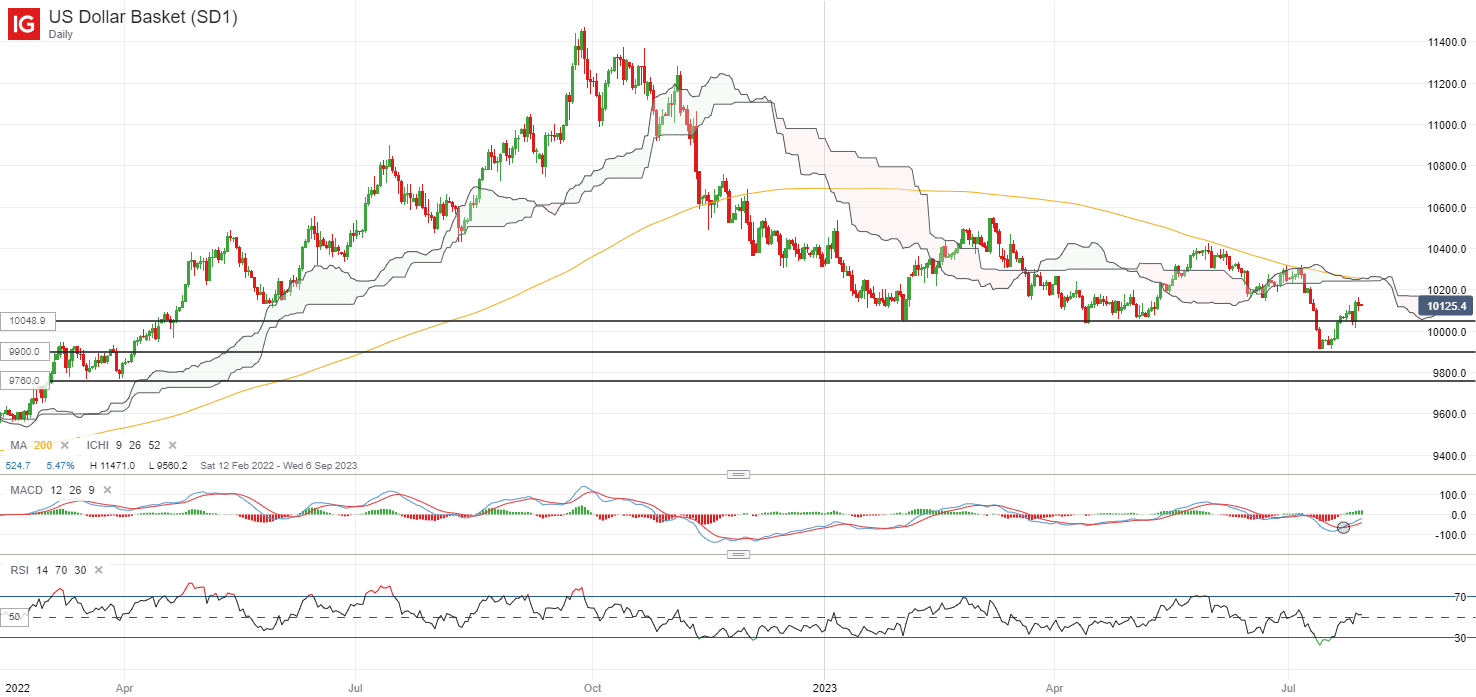

The US 10-year Treasury yields ticked 5 basis-point (bp) lower after touching its key 4% level in an earlier session. One on the radar may be the US dollar, which has displayed some resilience last Friday despite the lower-than-expected inflation readings. Thus far, the US dollar has defended its 100.50 level but much may still await, given that the lower-highs-lower-lows has put a downward trend in place. The relative strength index (RSI) is also back at its key 50 level, which could draw some sellers given that the dollar index has not been able to sustain above the 50 level since mid-June this year. The 100.50 level may remain as immediate support for some defending ahead.

Asia Open

Asian stocks look set for a positive open, with Nikkei +1.80%, ASX +0.24% and KOSPI +0.88% at the time of writing. Japanese 10-year bond yields continue to head higher to touch the 0.6% mark this morning, following the slight change to the Bank of Japan (BoJ)’s tone around its yield curve control (YCC) policy last week. While market participants seem to take comfort with the policy flexibility involved with the recent tone change, the higher risk-free rate has failed to dent the appetite in Japanese equities.

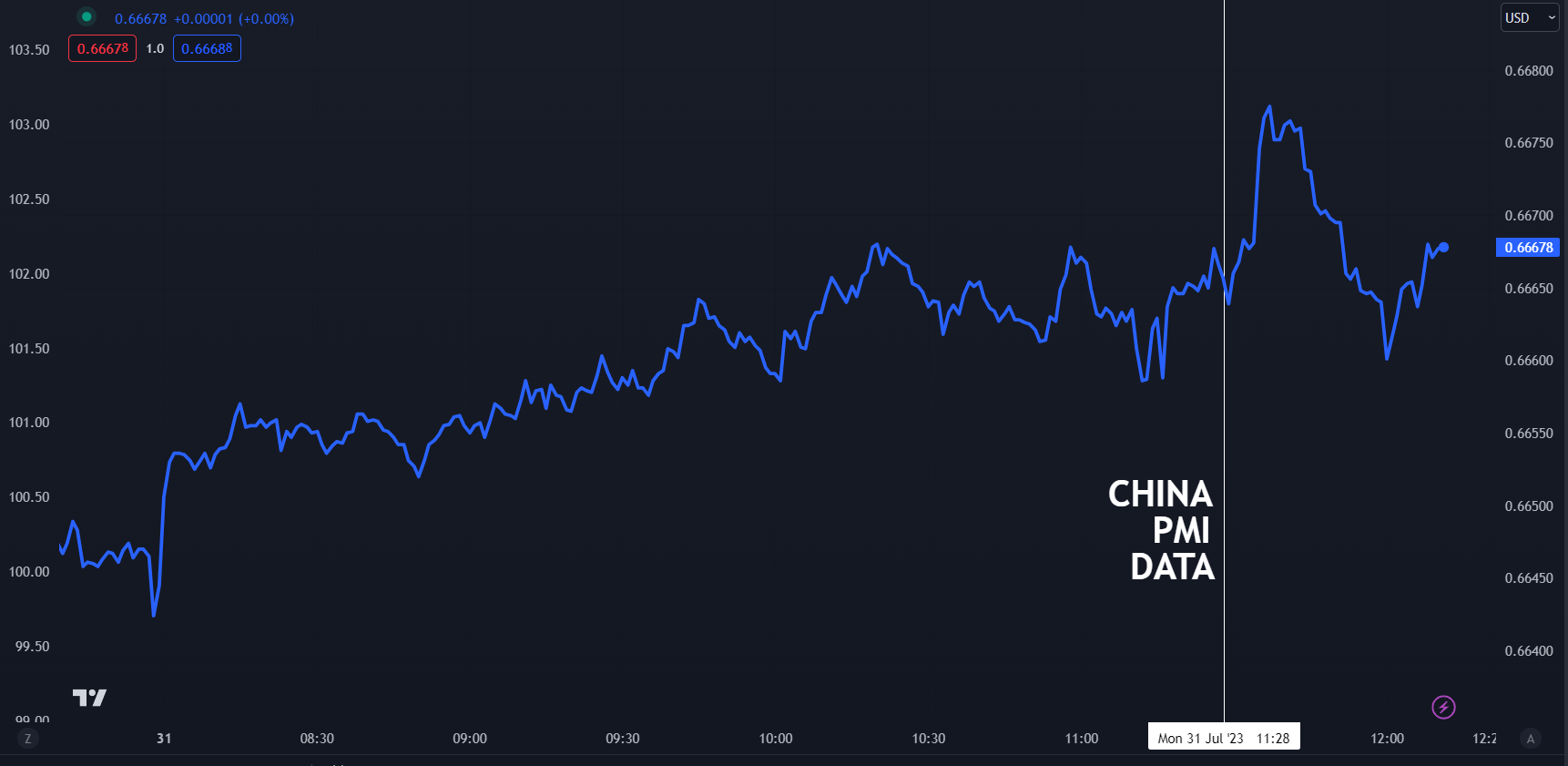

China’s Purchasing Managers’ Index (PMI) releases today came with another round of subdued read, with its manufacturing PMI at 49.3, a tick higher than the 49.2 consensus but nevertheless, still marked its fourth straight month of contraction. Reopening momentum for its non-manufacturing sector has tapered off quickly as well, with the non-manufacturing PMI coming in below expectations for the fourth straight month (51.5 versus 52.9 consensus).

The weak readings will further justify recent efforts by authorities to lift China’s growth picture, as market participants tread on some cautious optimism this morning, with the look-ahead to the upcoming new measures to boost consumption later today.

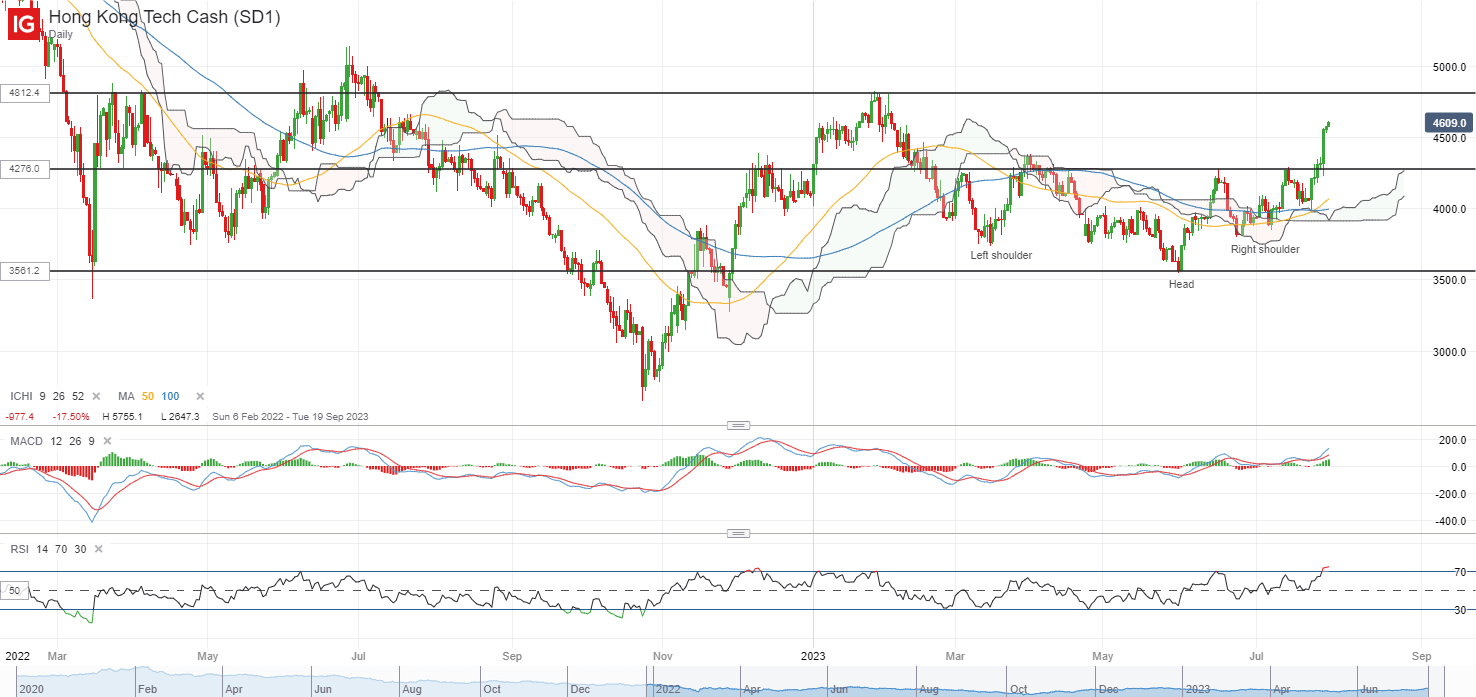

The Hang Seng Tech Index has displayed a minor inverse head-and-shoulder pattern lately, with a retest of the neckline last Friday met with a strong bullish move. Further upside may place the 4,812 level on watch next for a retest, where its previous reopening tailwind forms a peak back in January this year. Buyers have been taking some control lately, with its RSI defending the 50 level, along with a bullish crossover formed between its 50-day and 100-day moving average (MA). On the downside, the neckline at the 4,276 level may serve as immediate support.

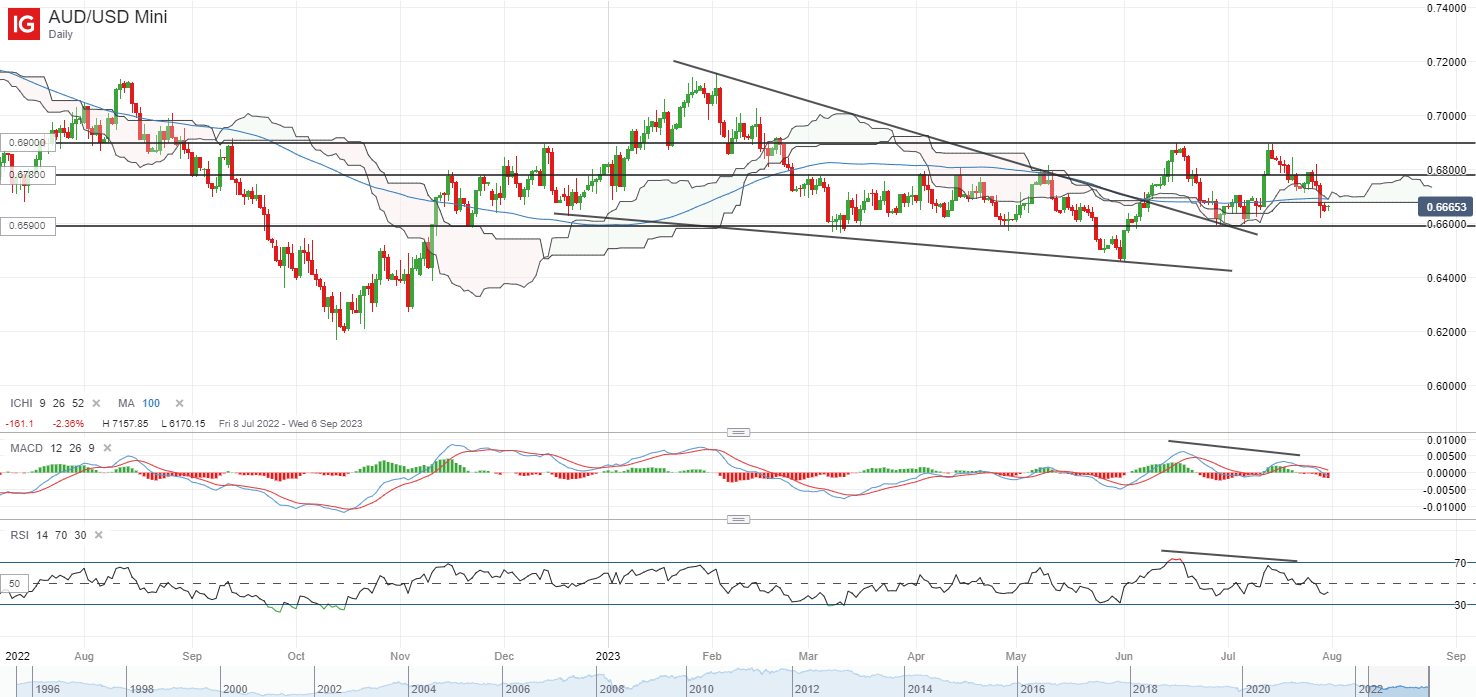

On the watchlist: AUD/USD on watch ahead of China’s stimulus, Reserve Bank of Australia (RBA) meeting

The AUD/USD has fallen by 3.7% over the past two weeks, as divergence in growth conditions between the US and Australia has been a key headwind for the pair, along with some firming in the US dollar lately. Thus far, past two interactions with the 0.690 level have not been met with a successful breakout, leaving a minor double-top pattern in place with the neckline support at the 0.659 level. On the upside, any positive reaction to the upcoming China’s stimulus announcement could leave the 0.678 level on watch for a retest, but greater conviction for the bulls may still have to come from a move above the key 0.690 level.

Given the downside surprise last week in Australia’s inflation (6% year on year versus 6.2% expected) and retail sales (-0.8% versus 0.0% expected), further wait-and-see are being priced for the upcoming RBA meeting. But with market rate expectations still pricing for a higher terminal rate at 4.35% (versus current 4.1%), guidance from the central bank will likely be the key focus.